Let me write about my own domain. Online grocery — e-grocery — is one of the hottest sectors in the world right now. Over 20 years after the failure of Webvan (the late-1990s US online grocery pioneer), true societal adoption is finally underway, and the real value of e-grocery is beginning to come into focus. I want to use five topics to capture the big picture.

1 / EC Penetration Is Rising Fast

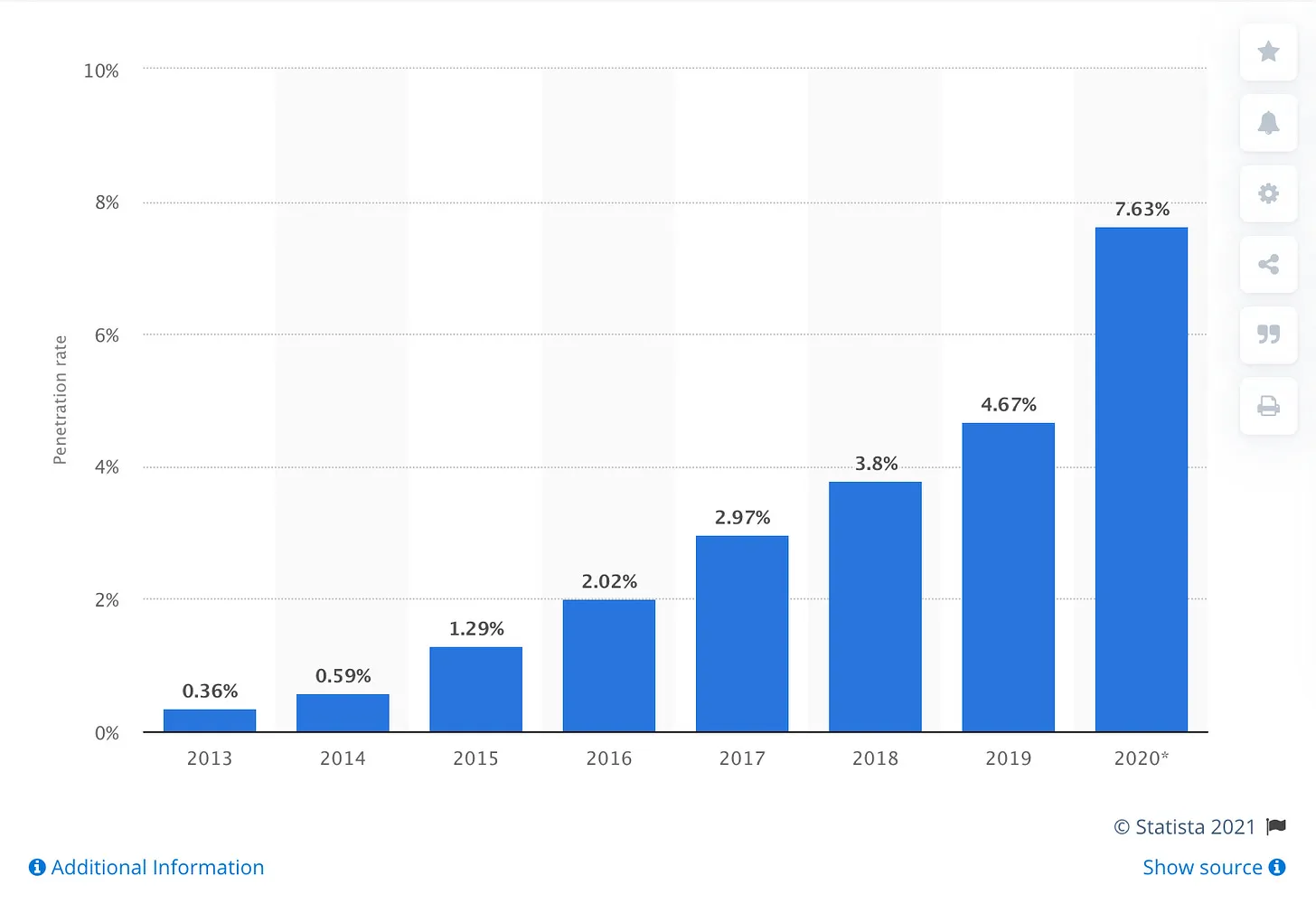

Japan's supermarket EC penetration rate sits at roughly 1–2% — extremely low. But in tech-advanced markets like China and the US, the picture looks very different.

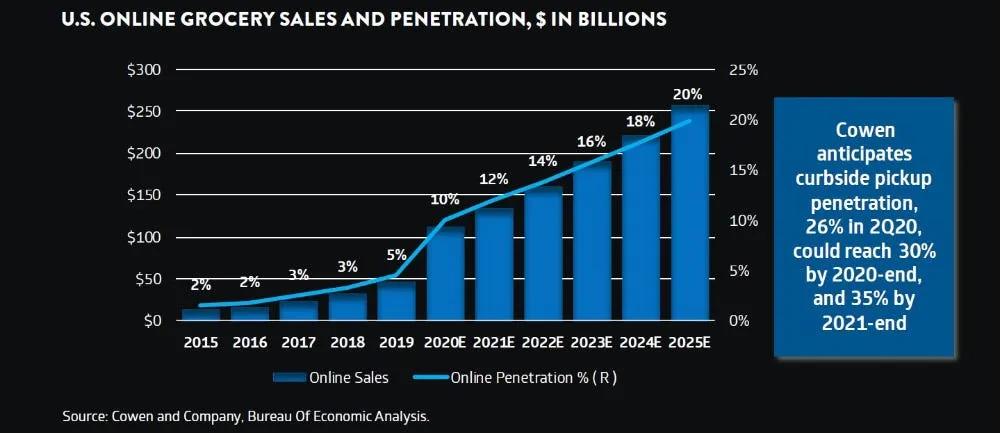

China saw grocery e-commerce penetration rise to nearly 8% in 2020 alone.

The US market roughly doubled in 2020, crossing 10% for the first time:

The drivers are highly local — the reasons China and the US got there are different. But COVID-driven demand acceleration was a common factor across markets. In Japan, demand was clearly strong, but unfortunately retailer supply couldn't keep up in 2020. We need to move faster.

2 / E-Grocery Is Among the Highest-Frequency Commerce Categories — Alongside Mobility

Uber announced the acquisition of Cornershop, an on-demand e-grocery service growing rapidly in Latin America. Go-jek and Grab are both strengthening their grocery verticals. Online grocery is recognized as "among the highest-frequency purchase behaviors" alongside mobility. Since COVID, it's been described as the hottest space in commerce.

3 / EC and Physical Stores Are Complementary, and Their Combination Increases LTV

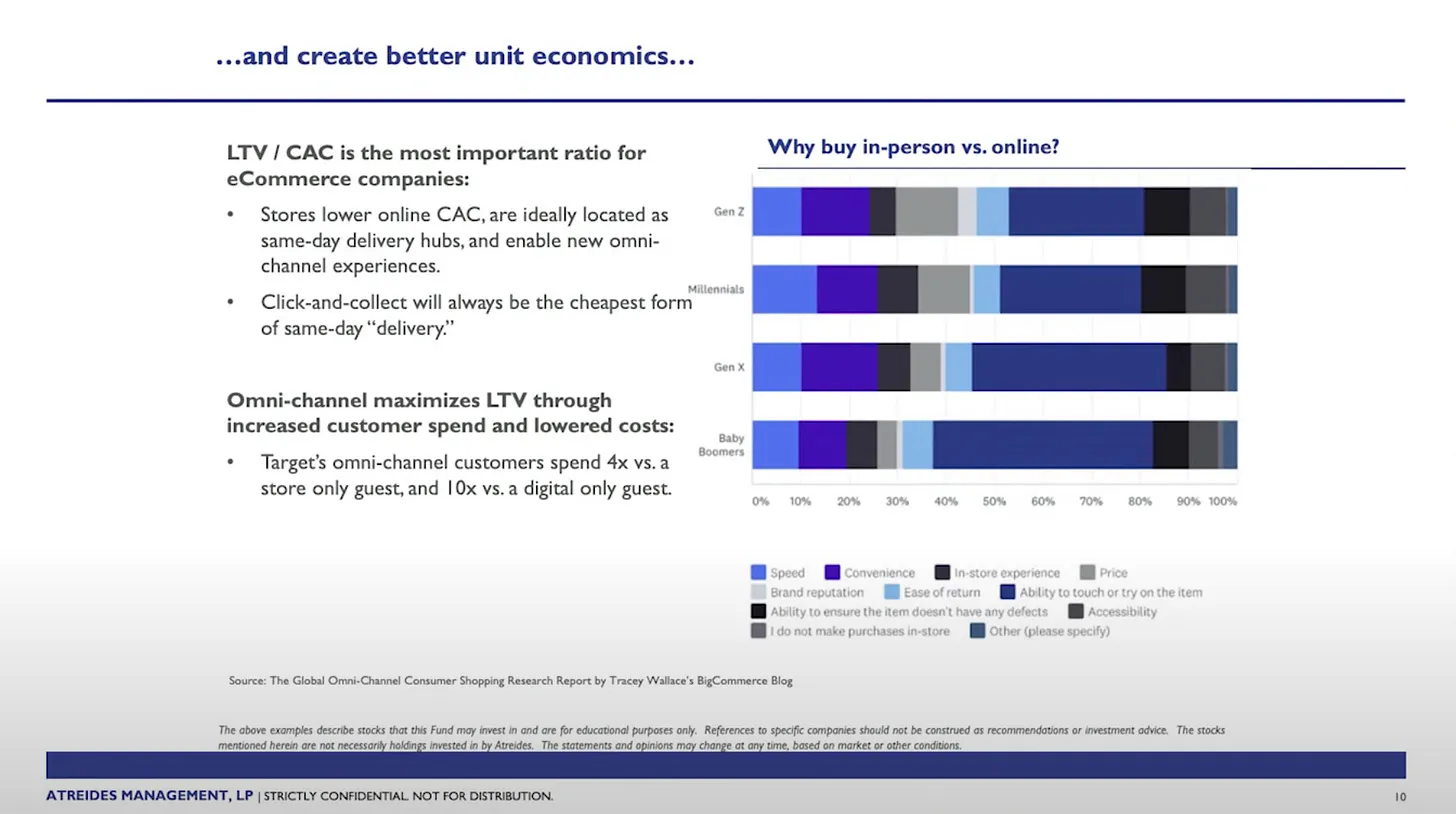

The following video provides a detailed breakdown of US Target's omnichannel growth strategy.

A key chart: customers who use both EC and physical stores generate 4x the revenue of store-only customers and 10x the revenue of digital-only customers. EC and stores don't compete — they amplify each other, dramatically increasing customer engagement.

4 / Click & Collect Delivers Striking Cost Reduction

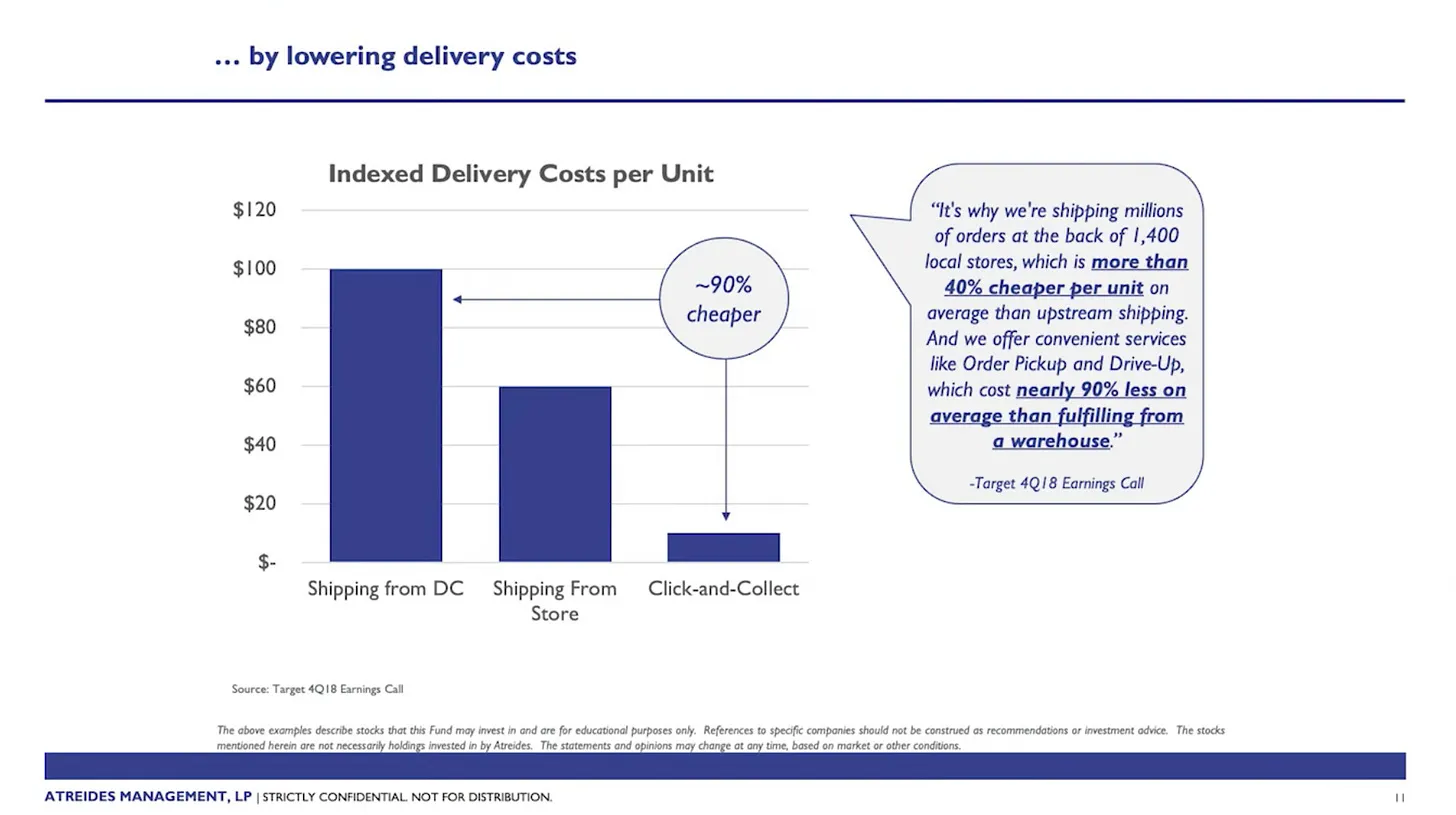

Another chart from the same Target video — comparing the cost of three fulfillment methods for their net supermarket. Warehouse fulfillment (shipping from a distribution center) is the most expensive. Click & Collect (customers order online and pick up in-store) reduces costs by nearly 90% compared to that baseline.

Click & Collect adoption is growing in Japan too. It started with food service chains — McDonald's, Starbucks — where per-order item counts are low. Supermarket adoption seems like a matter of time.

5 / The Pickup Model Is Gaining Ground

Pinduoduo — the Chinese social commerce platform — recently launched Duoduo Maicai, allowing customers to order online and pick up from local shops. Social commerce is converging with Click & Collect. Interestingly, this is essentially the same model as the Japanese consumer co-op "group delivery" system (班配送) that grew rapidly from the 1970s through the 1990s. (Japanese consumer co-ops operate a collective buying model where a local group pools orders and shares last-mile delivery — a well-established form of organized community purchasing.)

When 20 customers are delivered to in one trip, last-mile costs are reduced by up to 1/20. And customers only need to walk to a nearby pickup point, so the burden is minimal.

The pickup model also drives traffic to local stores — creating a local network effect that most pure-play EC platforms would find very difficult to replicate. This could become a meaningful new advantage for Pinduoduo.