This is a follow-up to my previous post on the technology that drove offline retail in Japan. There I tried to abstract the forces that shaped offline retail. Here I'll look at the actual trajectory of online retail (EC) in Japan, and ask: does the same law apply online?

What offline history teaches us

From the previous post, three principles emerged:

- The retailers who entered when traffic shifted to roadside strips in the 1980s–2000s became the dominant winners. Cars created a structural flow of traffic to roadside, and regional retailers who positioned there first grew enormous.

- Once roadside saturated and traffic patterns stabilized, the winners became fixed. Disruption has been rare since.

- In the saturation era, "one-stop shopping" — providing multiple categories and services in one place — became the growth formula. Convenience stores, drugstores, and Don Quijote are the models.

The law these three points reveal: retail growth depends on whether you can enter at the inflection point of traffic change.

No matter how innovative your store format or product offering, if you can't get into the path where people naturally move, you can't grow large. That's the offline retail lesson.

Understanding Japan's current EC market

First, let's establish the landscape of Japan's online retail as of 2018.

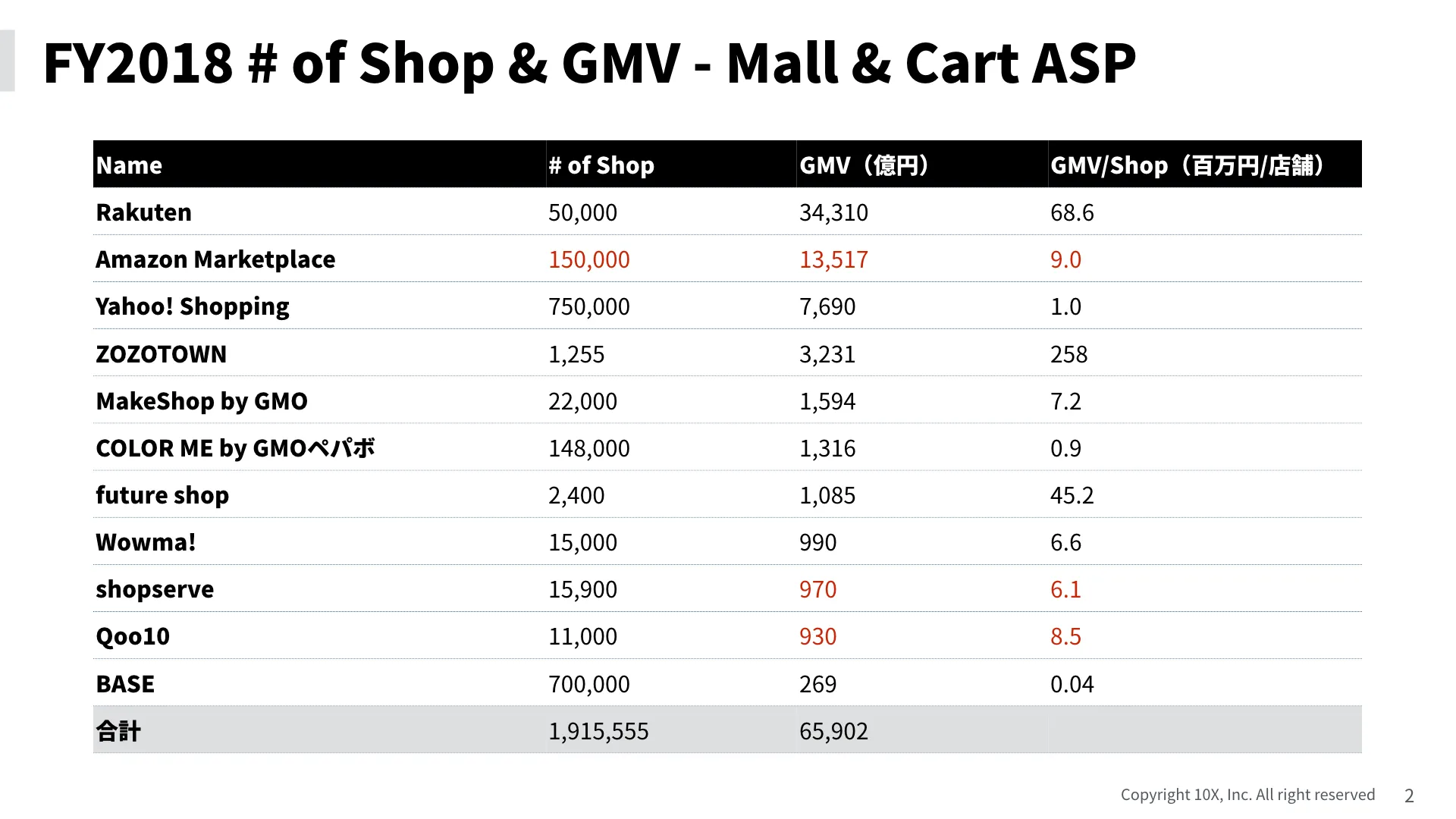

The table below shows the number of stores, GMV, and GMV per store for major mall platforms and cart ASPs (the SaaS services that let merchants build their own online stores).

Key facts:

- According to METI data, total physical goods EC GMV in Japan was approximately ¥9.3 trillion in FY2018.

- The combined GMV of the platforms listed above reaches ¥6.5 trillion.

Most of Japan's EC flows through merchants on roughly 10 platforms. Outside of those, FY2018 players exceeding ¥100 billion annually are limited to:

- Amazon Japan's own sales: ~¥1.25 trillion (author's estimate)

- Mercari: ¥346.8 billion

- Rakuma (Rakuten's flea market app): ~¥200 billion

- Yodobashi.com (large electronics retailer): ¥111 billion

A note on mall vs. cart ASP dynamics

About 2 million merchants use these platforms. Yahoo! Shopping and BASE each have around 700,000–750,000 shops. Both are designed for easy self-serve entry — no upfront cost, no sales process required. Perfect for individuals and small businesses.

Rakuten and ZOZOTOWN require passing through a sales and consulting process. They attract merchants with sufficient scale.

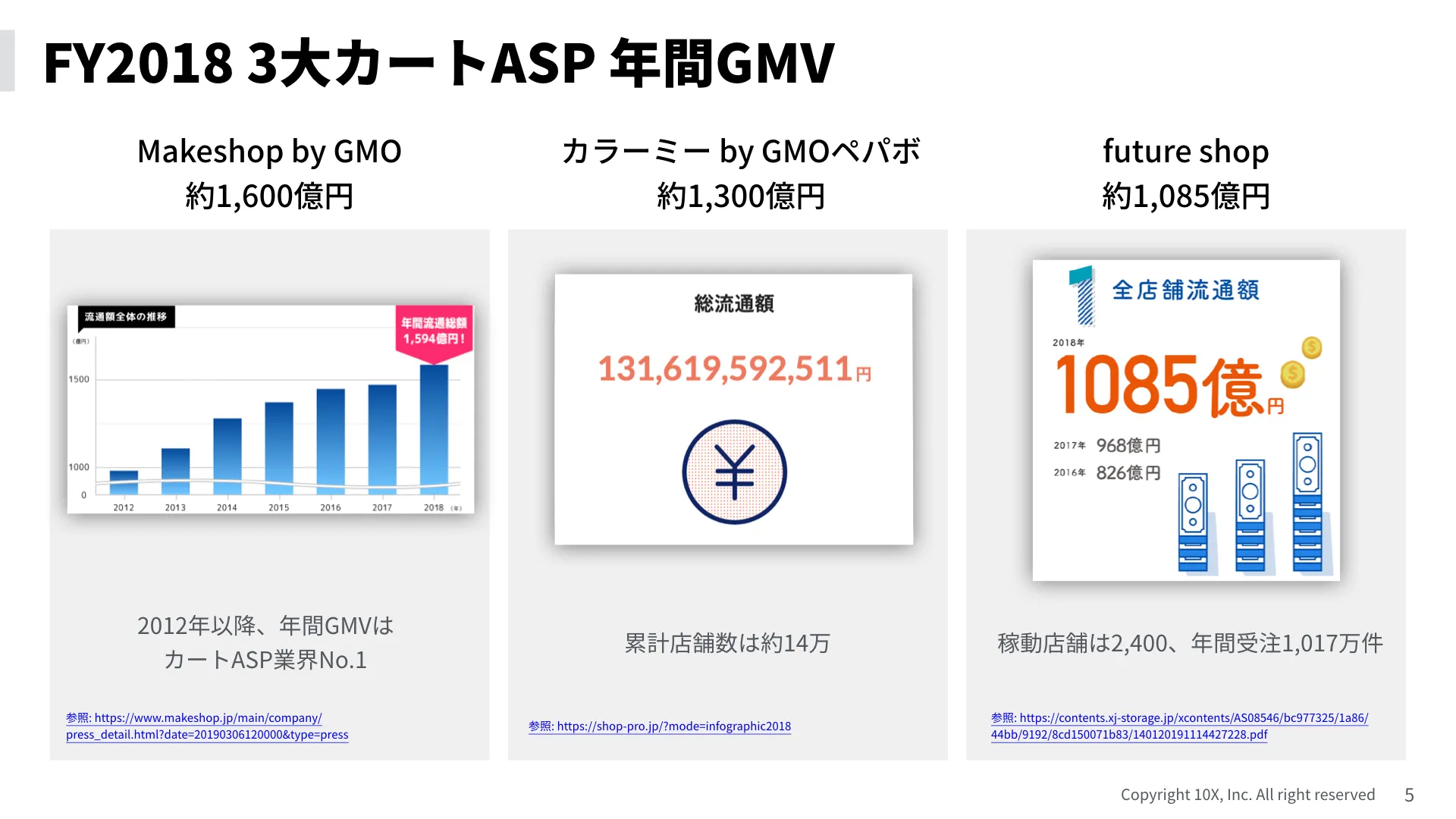

The three mid-tier cart ASPs (Makeshop, Color Me, Shopserve) each exceed ¥100 billion in GMV and are still growing. GMO Group owns both Makeshop and Color Me — combined, they move nearly ¥300 billion annually, a scale that rarely gets attention but is genuinely large.

Each platform looks similar on the surface, but they're actually finely optimized for different merchant size tiers. Merchants tend to migrate up the stack as they grow.

Shopify is now entering Japan and poses a genuine threat to all of these — with superior extensibility, competitive pricing, and strong global traction.

The history of Japanese online retail

Japan's EC history starts around 1995, when Windows 95 sparked an internet wave and many shops began using early mall services to sell online.

Rakuten Ichiba launched in 1996, building its business around mall-format EC (many stores in one place) and exploiting the "unlimited shelf space" advantage over physical retail. For over 20 years, it has remained Japan's dominant EC player.

Yahoo! Shopping and Yahoo! Auctions launched in 1999. Amazon Japan arrived in 2000, followed by Amazon Marketplace (its own mall format) in 2002. These three players — Rakuten, Amazon, Yahoo! — built Japan's EC history.

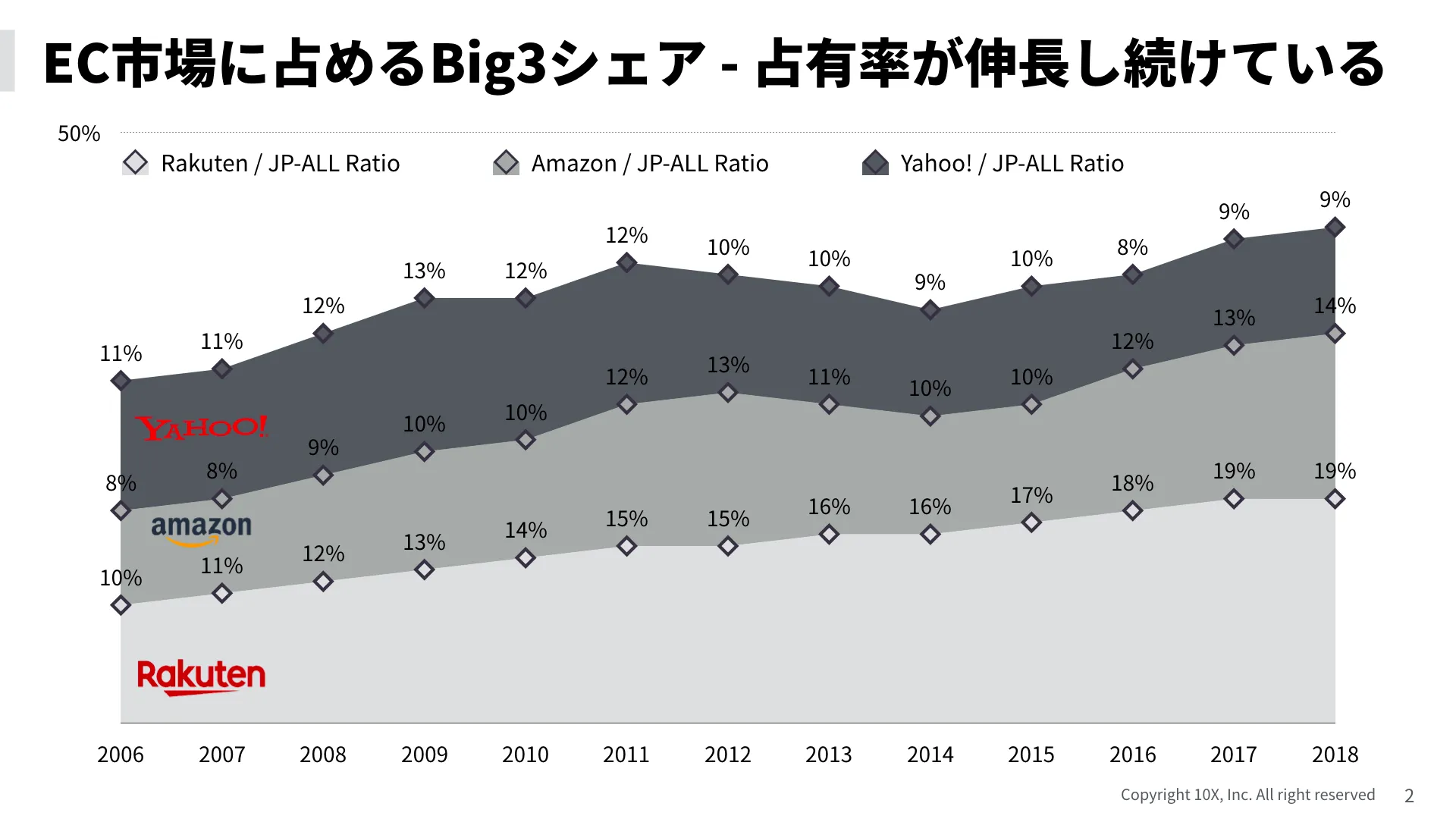

The chart below shows the share of Japan's total EC GMV held by these three from 2006 onward (based on METI data, company IR releases, and author estimates; Amazon figures include estimated assumptions; Yahoo! excludes ZOZO).

Looking at each individually:

- Rakuten: Never lost share. Has consistently grown faster than the overall market. ¥3.4 trillion GMV in FY2018.

- Amazon: Slowed mid-2010s but recently surpassed Rakuten's growth rate. ~¥2.6 trillion GMV in FY2018 (author estimate).

- Yahoo!: Peaked in the mid-2000s with Yahoo! Auctions, then fell behind on mobile and merchant acquisition. Relaunched by eliminating Yahoo! Shopping fees in 2015. Shopping is recovering while Auctions stagnates. ~¥1.6 trillion combined in FY2018.

By end of FY2018, the Big 3 held 43% of Japan's total EC market — and that share keeps growing. The market is moving toward oligopoly.

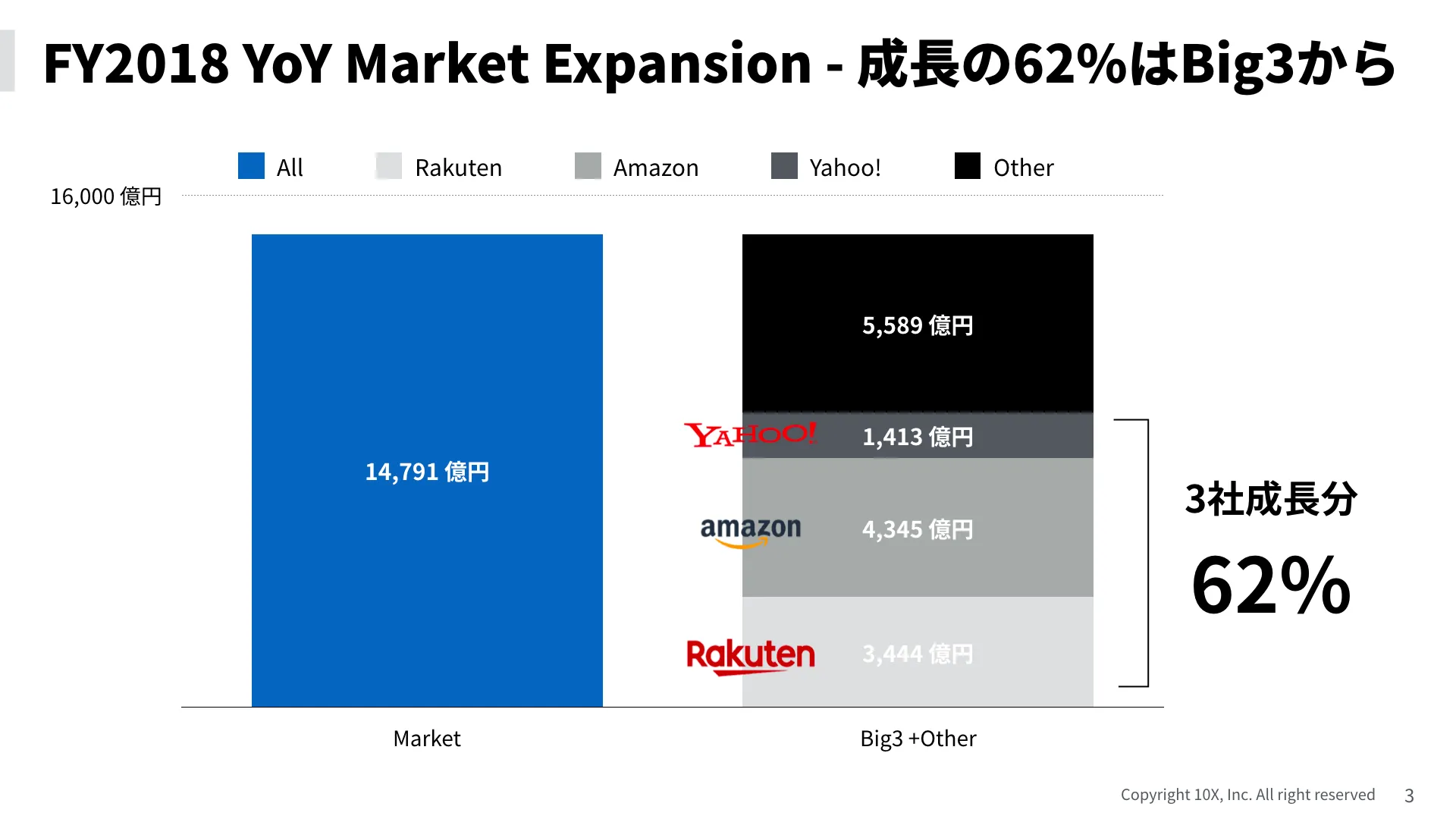

More strikingly: from FY2017 to FY2018, Japan's EC market expanded by about ¥1.5 trillion. 62% of that growth came from the Big 3 alone.

The offline pattern is repeating online: only the players who entered at the traffic inflection point became permanent winners.

Why did traffic concentrate in the Big 3?

Traffic to any website comes from three sources only — the online equivalent of "roads":

- Direct: User types or bookmarks the URL directly

- Referral: User follows a link from media, social, etc.

- Search: User queries a search engine and clicks through

Looking at Rakuten and Amazon via Similarweb, the vast majority of desktop traffic is Direct and Search.

What drives Direct and Search?

Direct traffic depends on UX — a user has to have had a positive enough experience to bookmark or remember the URL.

Search traffic has two types: branded search (the user already knows the name) and content discovery (they're searching for a product or topic). Both depend on whether the user can recall or encounter the brand.

In short: "prompted recall" and "UX" are the online equivalents of the car.

Search engines also evaluate UX. Rich product pages, high engagement, completed purchases, strong reviews — these signal quality. This creates a positive feedback loop: Amazon and Rakuten have deep trust signals, so they rank higher, get more traffic, get more reviews, rank higher. A smaller competitor with the same product literally cannot win on their own turf.

Why did this structure form? Because they entered when the internet was first spreading — before competitors could establish themselves. They captured search rankings, invested in UX, and locked in loyal users. Once those users established habits (Direct traffic) and trust (Search ranking), the structure became nearly permanent.

Today, research shows that consumers often search Amazon before searching Google for products.

Offline, new roads and new vehicles can occasionally reshape traffic. "Prompted recall" lives in human memory — it's much harder to displace. Online, structural change requires either a new channel or a new type of query (new product category).

The traffic inflection point: mobile and personalized media

There is one traffic shift underway: the rise of personalized media following smartphone penetration. Social media feeds, personalized search results, algorithmic recommendations — these have created a new kind of "bypass road" in online traffic.

The source of this bypass is personal preference. Users engage with content they like, and platforms surface more of it. This has enabled what I call niche commerce — high-price, specialized products reaching small but globally-distributed audiences at low cost.

Offline, a niche store on a side street couldn't get traffic. Online, before social media, a niche website faced prohibitive customer acquisition costs. Personalized social media changed this: narrow-but-deep preference groups can now be reached cheaply at global scale, making niche commerce economically viable.

In Japan, BASE is the platform most explicitly serving this: the lowest-friction way for a niche seller to open a shop. As tastes continue fragmenting and personalized media keeps evolving, this category will keep growing. (Mercari has a similar dynamic.)

Note: some categories — vegetables, staple food — resist preference personalization and don't fit the niche commerce model.

Looking ahead

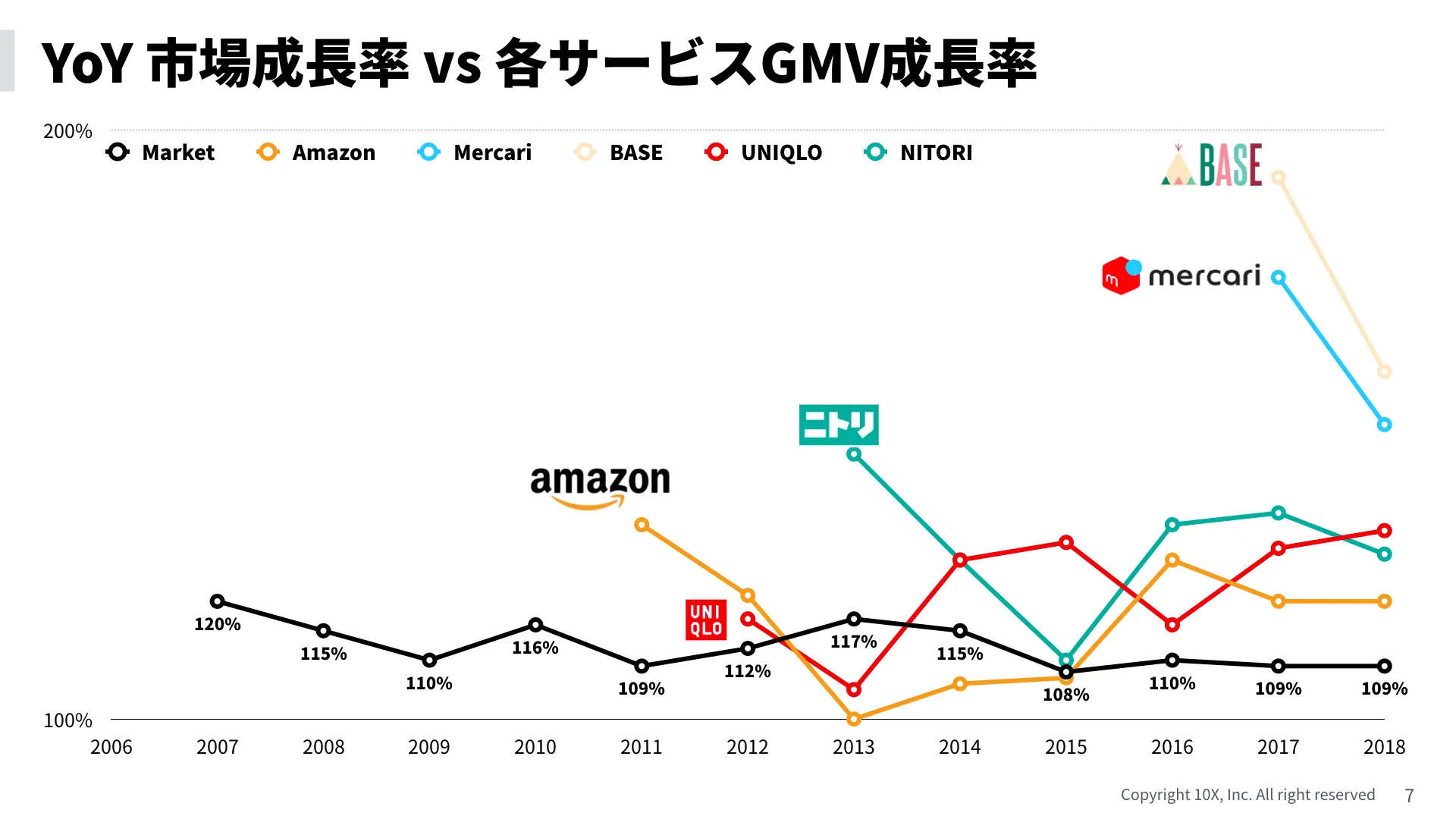

The chart below compares overall EC market growth with five specific services: Amazon, Mercari, BASE — and Uniqlo and Nitori (two major roadside retail winners).

Uniqlo and Nitori (a furniture and homegoods chain) are growing impressively. Yodobashi and Bic Camera likely show similar patterns (data not public).

The bottleneck for roadside winners going online was supply infrastructure and legacy systems tied to physical stores. But starting in the 2010s, the more forward-thinking among them began investing seriously in online. Uniqlo's Ariake Project is the flagship example — centralizing inventory for online, building logistics networks, building integrated systems and operations. The result is rapidly building "online supply capacity."

I believe the next major trend is the rise of named retailers online — established offline brands making serious moves in EC. They have something Amazon and Rakuten lack: brand-driven organic recall. Uniqlo customers search "Uniqlo" directly. That's a traffic asset that even Amazon can't buy.

This is already happening in the US: Walmart's acquisition of Jet.com was the turning point that gave them the online infrastructure to leverage their massive offline trust and distribution network. The Walmart vs. Amazon dynamic in the US is a useful lens for predicting Japan's future.

Summary

- Japan's EC market is dominated by merchants using mall and cart ASP platforms, with Rakuten, Amazon, and Yahoo! (the Big 3) holding 43% share and growing.

- The offline law — retail growth depends on entering at the traffic inflection point — applies more strongly online. "Prompted recall" as a traffic source is even harder to displace than physical location.

- Mobile-driven personalization has created a new traffic structure enabling niche commerce. This trend will continue.

- The next major trend will be the rise of named (established) retailers in EC, leveraging their offline-built brand recognition and organic search.

Next I'll look at OMO (Online Merges with Offline) in Japan through this lens.