This post examines the background behind OMO (Online Merges with Offline) — the approach Jack Ma branded "New Retail" in China — and asks why it happened. My argument: the forces that drove OMO in China are fundamentally different from what's needed to move Japanese retail forward. China-style OMO is not a playbook Japan should copy.

Background: the "time machine" problem

Over the past five years, there's been a wave of startups in Japan importing business models that worked in China — live commerce, bike sharing, ride sharing, mobile payments, cashierless convenience stores, mobile-order-first restaurants. The implicit theory is that Japan is a few years behind China, so Chinese playbooks will work here with some delay.

I've been skeptical. Particularly in retail × technology, the forces that will advance Japanese retail are fundamentally different from Chinese ones. Approaches like "stores designed around mobile-native customers who don't need to visit in person" — which look successful in China — are unlikely to have a huge impact in Japan.

What is New Retail?

"New Retail" is a strategic concept proposed by Alibaba founder Jack Ma in October 2016:

New Retail — the integration of online, offline, logistics and data across a single value chain.

In practice, Alibaba's New Retail strategy breaks into two distinct business types:

1. Physical retail for mobile-native customers

This is the type that gets attention in Japan: using mobile-first, data-driven operations to build stores that don't require traditional in-person shopping behavior.

The flagship examples are Luckin Coffee (瑞幸咖啡), which IPO'd on NASDAQ just 18 months after founding in May 2019, and Hema Fresh (盒馬鮮生), an Alibaba-backed supermarket chain.

Hema connects the mobile app, in-store experience, and online ordering seamlessly. Customers can shop in the store, eat at the food court, or order delivery — and delivery arrives within 30 minutes. By August 2019, Hema had 160 locations and announced a target of ¥16 trillion in GMV over 10 years.

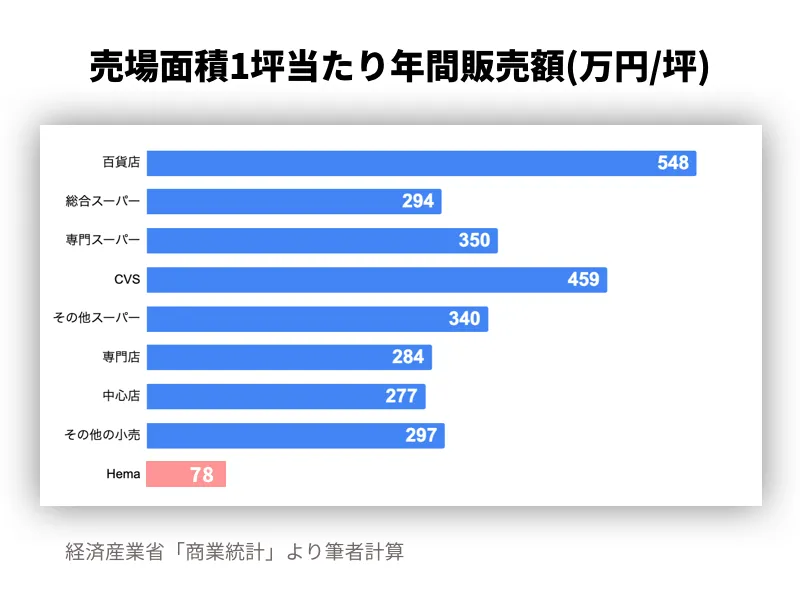

Hema's per-tsubo (approximately 3.3 sqm) sales average is often cited as more than 3x the Chinese competitor average. However, this benchmark pales against Japanese specialty supermarkets, which average roughly ¥3.5 million per tsubo — Hema is at less than a quarter of that.

Hema is not producing extraordinary KPIs. It's an interesting format but still has significant room for economic improvement.

2. Digitization platform for small independent stores

This second type gets much less attention in Japan, but in terms of scale, I believe it's the more strategically significant one. The flagship is Alibaba's Ling Shou Tong (LST) (零售通).

LST is a platform that digitizes the 6 million small independent stores and "mom-and-pop shops" that make up about 70% of China's retail. Alibaba provides these stores with access to the data and tools it developed for its own OMO operations.

By the time I'm writing this, LST has been adopted by 1.3 million stores — about 22% of its target market — and consolidation is beginning. The three-sided value of the platform:

- Independent stores: Alibaba automatically generates lists of products likely to sell well in that store. Merchants can order hot-selling items directly from Alibaba's central warehouse via a dedicated mobile app. Merchandise planning is automated; promotions are maximized.

- Consumer goods manufacturers: For the first time, brands can reach 1.3 million small stores that were previously impossible to market to. "Connect a great product to LST and it gets placed in the optimal stores" — reach expands automatically.

- Alibaba: Gains ID-level POS data from a massive offline store network, improving its models. Logistics scale economics keep delivery costs low. GMV share grows.

LST feels structurally similar to how Japanese convenience store franchises work: the parent company expands its network through store owner contracts, then provides both proprietary products (developed using nationwide sales data) and promotional tools. LST is essentially a digitally-sharpened version of the franchise model, opened up to non-franchise independent stores.

Why OMO happened: two root causes

Over the past decade, China developed the world's fastest-growing mobile EC ecosystem. This created two structural problems:

Rising customer acquisition costs

As mobile users converted to e-commerce shoppers at speed, CAC skyrocketed:

Alibaba

- September 2013: 12.17 yuan/user

- December 2018: 77.99 yuan/user

- 6.45x increase in 5 years

Pinduoduo (group-purchase EC, Tencent-backed)

- Q2 2017: 1.95 yuan/user

- Q4 2018: 54.71 yuan/user

- 28x increase in 18 months

When CAC exceeds a sustainable range, unit economics break. Tech giants needed to invent lower-CAC customer touchpoints.

The unreachable 800 million

China's mobile internet reached approximately 800 million users in about 10 years — a remarkable penetration. But that still left roughly 800 million people, largely in rural areas, who weren't yet mobile commerce users.

These two problems — soaring CAC for already-online users, and unreached rural populations — are likely the core drivers behind OMO. Creating physical stores for mobile-native customers was a lower-CAC touchpoint. Digitizing existing small stores was a way to reach dispersed populations efficiently.

China's lack of cars matters enormously

There's a structural difference between China and Japan that makes the Chinese OMO playbook non-transferable.

Japan's offline retail development was driven by car ownership (see my earlier post on this). Cars created traffic on roadside strips; the retailers who captured that traffic in the 1980s–2000s became the dominant winners.

China's situation is the inverse. Mobile internet penetration was effectively complete before car penetration. As of 2017, car ownership in China was only about 15% — compared to Japan and the US at 60%+ levels. For China, cars are still an emerging trend, not a foundation of retail traffic.

In Japan and the US, roadside large-format stores efficiently collect traffic because most people travel by car. In China, there's no equivalent dominant offline traffic point — which is partly why 6 million small independent stores still survive and haven't been consolidated.

LST's network-building and DX approach is efficient precisely because reaching dispersed populations through offline stores is more practical than through roadside large-format retail in China's geography and car ownership reality.

Conclusion: OMO was the strategy for capturing the next traffic inflection point

Throughout this retail series, I've argued that retail growth depends on being able to enter at the inflection point of traffic change.

China's traffic inflection point over the past decade was clearly mobile internet — and players rushed in. But that opportunity is now saturating. The next inflection point is being sought in offline.

OMO — mobile-native stores and digitizing distributed small stores — was the strategy for capturing that next offline inflection point.

There are also social underpinnings that make OMO viable in China but not elsewhere:

- China has had a nationwide citizen ID system for nearly 30 years, making identity verification almost frictionless. This has driven mobile payment and financial services adoption.

- A roughly 7x wage differential between rural migrant workers and urban professionals provides an abundant, affordable supply of pickers and delivery riders for services like Hema.

OMO is a product of these specific conditions. Japan has nearly opposite conditions across most of these dimensions. "What worked in China" is not a reliable playbook for Japanese retail.